Knowledge is power and the latest Department of Labor statistics can help brokers pinpoint coverage gaps in ancillary benefits

Many insurance brokers know The DBL Center for our expertise in mandatory disability insurance and paid family and medical leave. But our ultimate goal is to help brokers boost their commissions by helping their clients privatize required benefits and roll the cost savings into closing other risk gaps.

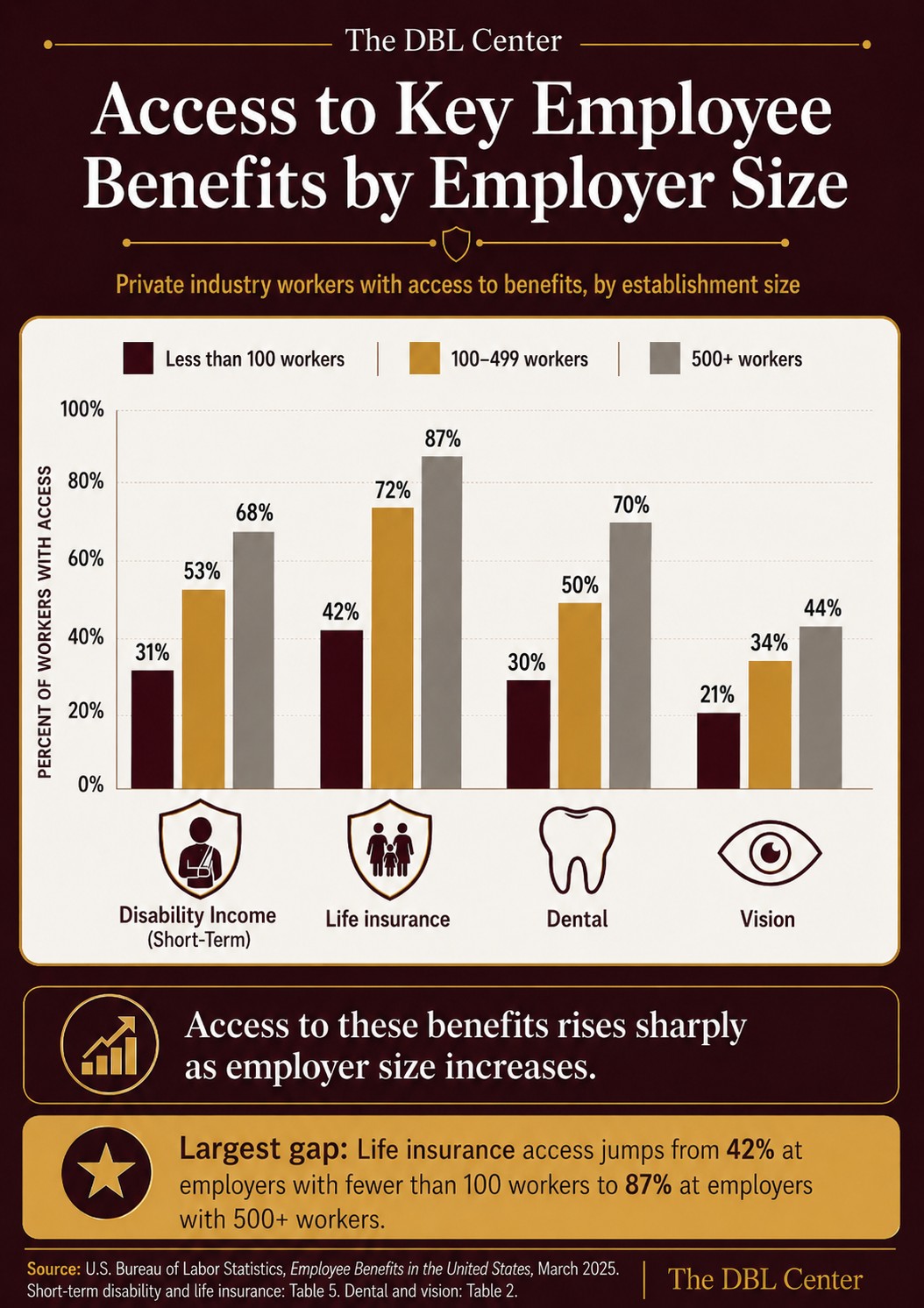

Understanding what employee benefits are available to US workers, what sectors are lacking benefits, and what benefits are most in-demand helps brokers become trusted partners to their clients.

Life Insurance Shows High Take-up Rates

A survey from 2024, reported by The DBL Center, revealed that 59% of Americans would be willing to cancel their Netflix subscription, $15 per month at the time, to purchase a life insurance policy that would protect their family financially.

That sentiment remains, exemplified by high take-up rates when employers offer Group Life / AD&D coverage. Across all types of employers, including civilian, private industry, and state and local governments, 68% offered life insurance, with an average take-up rate of 98%, according to recent BLS data.

Access was highest with government employers, at 84%, while 62% of civilian employers and 59% of private employers offered life insurance.

This chart shares a breakdown of life insurance offerings by industry.

What This Means for Insurance Brokers

If employers aren’t offering life insurance, they’re neglecting an important recruiting tool, especially if they’re a larger employer. Life insurance access more than doubles with employers with more than 500 lives.

With take-up rates close to 100%, executive carve-outs to give high earners the coverage they need, and generous commissions, Group Life is one of the key benefits brokers should be offering to their clients.

Seventy Percent of Small Employers Don’t Offer Dental Coverage

Dental coverage was previously part of many medical insurance plans. But as health insurance rates increase and coverage levels fall, some plans are dropping dental from healthcare offerings.

This represents a tremendous opportunity for brokers to offer an in-demand benefit on a voluntary or cost-shared basis.

Only 30% of small businesses under 100 lives offer dental coverage to employees, but 70% of businesses with 500+ workers offer the benefit.

What This Means for Insurance Brokers

There are opportunities within small and larger businesses to privatize mandatory benefits and roll that cost savings into a dental plan. Dental coverage frequently emphasizes preventative care, which can reduce absenteeism and improve employee productivity through better holistic health.

Vision Coverage

As with dental insurance, vision coverage used to be part of many healthcare plans. Today, fewer than half of employers of every size offer vision coverage. Yet, 75% of American adults need vision correction; 64% wear prescription glasses, according to data from the Glasson app.

Employers who don’t offer vision coverage are missing an important opportunity to give their workers a needed, money-saving perk that can also help boost productivity.

What This Means for Brokers

Vision coverage is an affordable upsell that can be offered on a voluntary, employer-funded, employee-funded or cost-shared basis.

Presented as part of a full employee benefits package that also features dental coverage, vision insurance puts money in your pockets and helps employees keep more of what they earn with discounts on eye exams, glasses, and more.

Disability Income

Even in states where group disability or paid family and medical leave aren’t mandated, the majority of employers with over 100 lives offer short-term disability benefits to workers.

This figure drops to less than one-third (31%) for employers with less than 100 lives, showing a critical risk gap.

What This Means for Brokers

Short-term disability is an important benefit to help employees maintain their financial stability in case of an off-the-job injury or illness. Growing numbers of states are mandating short-term disability in the form of paid family and medical leave.

Encourage your clients to explore private policies in these states for cost savings and easier claims management. Employers in New York should enrich DBL coverage beyond the state maximum of $170 per week.

Reach out to The DBL Center team for an analysis of your clients’ risk gaps and explore ways to expand your book of business with bundled ancillary benefits.