Don’t leave money on the table if you’re writing business for under 50 lives in New York

You don’t have to wait for the state to make a decision about Senate Bill S172, which would bring DBL pay more in line with Paid Family Leave benefits in New York. You can help your clients enrich DBL benefits now.

Under the Disability Benefits Law in New York, many employers are already withholding the maximum allowable amount of $31.20 per year. But if an employer writes their DBL insurance through a private plan, they might be paying less than that in annual premiums. They can roll that cost savings into enriched DBL benefits and ancillary benefits.

Why Enrich DBL Insurance?

By working with The DBL Center to help your clients enrich DBL and bundle a complete package of ancillary benefits, you’ll help your clients close risk gaps and boost your commissions.

Robust employee benefits packages have been shown to improve recruiting and retention. This is especially important in highly competitive regions like the New York tri-state area, where New York businesses may compete with New Jersey and Connecticut for top talent.

Working with The DBL Center for NY DBL Enriched options gives brokers access to exclusive connections with our partner carriers. Through our network of relationships, we can help you provide your clients quality insurance to be successful and compliant.

Examples of Enriched DBL Coverage Costs for Employers

If an employer begins taking the NY DBL payroll deductions as it allows under the law (WKC Chapter 67, Article 9 § 209.1-3), then the employee would contribute $31.20 per year. Your client (the employer) can redirect their employer-funded $31.20 into enriched coverage.

Here are a few examples:

- Carrier A: offers a 2x benefit plan max benefit of $340/week with extra if they go into the hospital raising their weekly benefit to $510/week. The cost is $33.00 annually for males and $72.00 for females.

- Carrier B: offers up to $749 weekly benefits at 60% wage replacement for $0.338/males and $0.548 females.

Tremendous Opportunities for Clients with Under 50 Lives

If you’re an insurance broker with clients in New York, it makes sense to review their employee benefits plans now, before the state makes a decision on enriching DBL coverage.

For businesses with fewer than 50 lives, especially if the majority of workers are males, who often have lower premiums, the cost savings with a private plan can be substantial.

“For heavy male groups, especially, allowable employee withholdings can pay for some enriched benefits. Brokers need to be having conversations now about employee contributions,” said DBL Center CEO and growth leader Michael S. Cohen.

“If New York does finally increase benefits, the conversation about employee contributions will come up. Brokers have an opportunity to talk about it now, before business owners and benefits advisors are thinking about it,” he said.

For more than 40 years, The DBL Center has been on the leading edge of mandated employee benefits. We are here to help our brokers lead the conversation surrounding NY DBL law with their clients.

Will New York State Provide a Disability Benefits Increase – 2026?

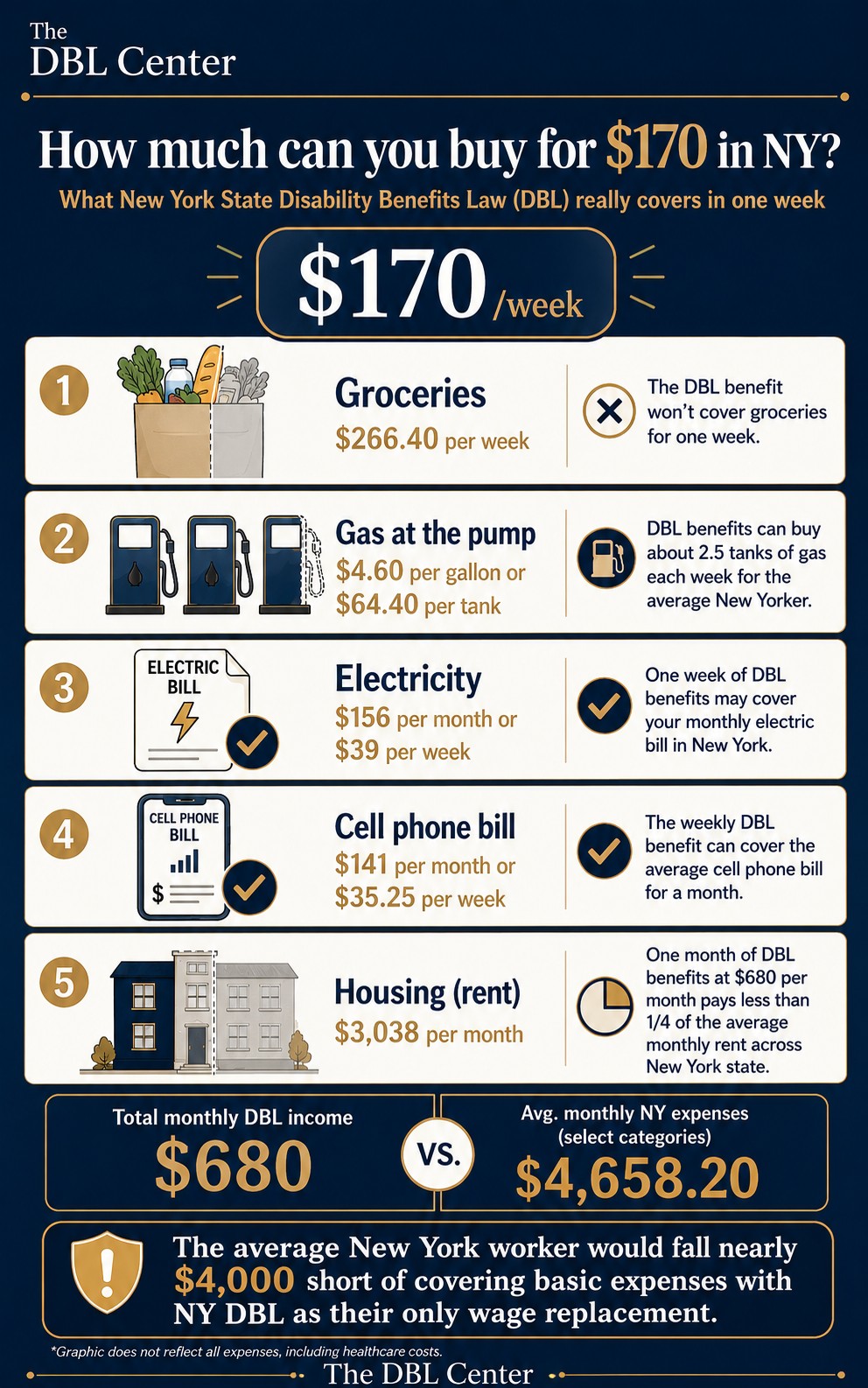

For decades, the maximum benefit for DBL in New York has been stuck at $170 per week. Teenagers working at McDonald’s earn more than that. Yet, legislation that would increase the DBL benefit to a livable amount remains stuck in Albany.

New Yorkers who need to file a claim for an off-the-job illness or injury can’t make ends meet, pay their mortgage or other bills on $170 per week. That amount barely covers groceries in more expensive regions of the state.

Right now, S Bill S172A passed in the Senate, but there are still many steps before it’s signed into law.

If enacted, the bill would “increase TDI benefits in parity with Paid Family Leave,” according to the NY Senate website. Increases would be phased in over several years. Once fully phased in, benefit amounts would be adjusted annually in line with the state’s average weekly wages.

What You Can Do About Senate Bill S172 Now

It’s in brokers’ best interests to see Bill S172 signed into law by the New York State governor. Higher premium costs equal larger commissions. More importantly, increasing the DBL benefit helps workers and keeps New York fiscally strong.

Write to your state legislators and voice your support of the bill to increase DBL benefits. You can also visit the Senate website and click “aye” for Bill S172a.

Next Steps to Help Your Clients Enrich DBL

While we wait for final actions on Bill S172, it’s time to start conversations with your clients around enriching DBL and what employers may expect in the future. If NYS increases the benefit, your clients will already be aligned to take the next steps toward compliance. The DBL Center is here to help.

The first step is to obtain a census of employees, male and female, from your clients in New York (or with employees in New York) with under 50 lives.

The DBL Center will shop the policy to our network of private carriers and come back with quotes for enriched policies. We can help your clients roll the cost savings of a private plan into ancillary benefits.

You’ll gain the advantages of access to our proprietary Broker Dashboard: Net Revenue Tracker and white-glove service from our knowledgeable team. We’re your back-office staff for mandated and ancillary employee benefits, so you can help your clients save money and build a more robust benefits package.

FAQs

What is the difference between DBL and PFL?

DBL in NY provides eligible employees with up to 26 weeks paid leave for an off-the-job injury or illness, with a maximum benefit of $170 per week. PFL, or Paid Family Leave in NY provides up to 12 weeks of leave to care for a family member with a serious health condition, to bond with a newborn or newly adopted or foster child within the first year, or for a spouse’s military exigency.

Is DBL required in NY?

The State of New York workers compensation board and NYS Department of Labor require most private businesses with employees in the state to provide disability benefits. Businesses can purchase benefits through a state plan or a private insurance carrier.

What is the maximum DBL benefit in NY?

The maximum DBL benefit in NY in 2026 is capped at $170 per week. Insurance brokers can help their clients enrich DBL coverage with higher amounts, better service, and a smoother claims process with just a small premium increase.