Colorado Paid Family Leave

Colorado Paid Family Leave, known as the Colorado FAMLI (Paid Family and Medical Leave Insurance) program, is set to go into effect January 1, 2024.

This program will provide paid benefits to employees who are unable to work temporarily due to illness or injury or need time off to care for a family member with a serious health condition or to care for a new child within the first year of birth, foster care, or adoption.

It’s important for business owners in Colorado to begin planning now for Colorado FAMLI to go into effect. Colorado is following in the steps of New York, New Jersey, Massachusetts, and Connecticut and permitting business owners to write their FAMLI plans through a licensed insurance broker in the state, which means cost savings for business owners and an expanded revenue stream for DBL Center brokers.

We will help you tap into this new market with all the information you need regarding Colorado paid family leave.

What You Need to Know About Colorado FAMLI

First, you’ll want to understand the specifics of Colorado Paid Family Leave, who is eligible for it, and how much the benefits pay.

According to the Colorado Department of Labor and Employment website, organizations with their own paid leave program that is better than what the state mandates may apply for an exemption. Every company and organization in the state must provide paid leave. Premiums will equal 0.9% of an employee’s wage.

Small businesses with fewer than 10 employees do not have to contribute to the program. They must remit the employee’s share of 0.45% quarterly, with those funds coming from payroll deductions.

Employers with more than 10 workers must cover one-half (0.45%) of the premium, while employees cover the balance through payroll deductions. Employers will need to begin submitting premiums to the CDLE by January 1, 2023.

Who Can Claim Colorado FAMLI?

Colorado’s family leave benefits mirror those in other states, permitting employees to take time off to care for a new child within the first year of birth, fostering or adoption or to care for a family member with a serious health condition.

Colorado FAMLI also provides paid leave for an employee unable to work due to illness or injury incurred off the job. Paid leave also extends to employees who need time off to make arrangements for a family member’s military deployment or to address immediate safety needs and life changes following domestic violence or sexual assault.

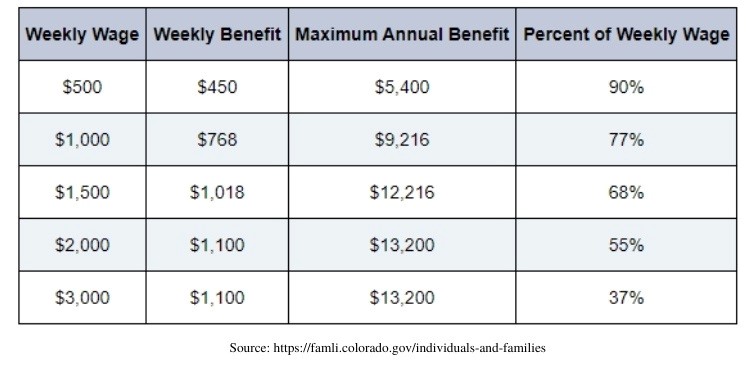

Colorado FAMLI pays as much as 90% of an employee’s weekly wage, based on income. You can see from the chart below that employees earning an average of $500 per week will receive 90% of that wage, up to a maximum annual benefit of $5,400.

The percentage of weekly wage received drops as salaries increase. Individuals earning $3,000 per week or more will take home a weekly benefit of $1,100 with Colorado FAMLI, or 37% of their weekly wage, up to a maximum benefit of $13,200 annually.

FCA v. FAMLI: Who Is a Family Member Under Colorado FAMLI?

It’s important not to confuse Colorado FAMLI with the state’s Family Care Act. Colorado FCA Colorado’s provides job protection and unpaid leave for up to 12 weeks of leave to care for a family member.

Under the FCA, Colorado defines a family member as a parent, child, or spouse, as well as a domestic partner or civil union partner. It is likely that FAMLI guidelines will follow the same definitions, although Colorado may expand the definition of a family member in the same way Connecticut did. Connecticut defines a family member as any blood relative, or anyone whose close association to the employee is the equivalent of a family relationship.

How Brokers Can Explore Colorado Paid Family Leave as a Revenue Stream

For insurance brokers who are already offering private DBL in New York, TDB coverage in New Jersey, or FMLA in New England states, Colorado Paid Family Leave represents an opportunity to enter a new market by sharing your expertise and leveraging your relationship with The DBL Center to provide the best coverage, top-quality service, and cost-savings on premiums by bundling paid family and medical leave with ancillary benefits.

As your back office staff, The DBL Center has the relationships with top carriers to provide concierge-level service to your clients. Our DBL Center brokers also have access to our proprietary Broker Dashboard: Net Revenue Tracker to track renewals, cancellations, and commissions easily.

As an insurance broker, once you get your foot in the door to guide Colorado business owners through the process of implementing a paid family leave program, you can introduce them to ancillary benefits, too.

By bundling Colorado FAMLI benefits, if possible, with ancillary benefits such as vision, dental, long-term disability (LTD), group life / AD&D and accident insurance, you can increase your commissions while increasing your value to your customers.

You’ll save Colorado business owners money at a time when everything seems to be increasing in price and business owners face more challenges than ever.

By privatizing Colorado Paid Family Leave, business owners won’t need to remit contributions for the first year of premiums to the state. Now is the time to write Colorado FAMLI because business owners will never see that first year of savings again.

Benefits of Privatizing Colorado Paid Family Leave

Colorado business owners see tremendous benefits by privatizing paid family leave instead of writing their benefits through the state. First, if an employer secures a private policy before January 2023, when the first payments would be due to the state, they can avoid that first year of premium payments.

Additionally, private insurance plans such as New York State DBL or New Jersey TDI offer faster, more flexible payouts and better customer service. By working with a licensed broker, Colorado business owners and their HR staff will have a knowledgeable team working to help them through the claims process. They can also help them secure the lowest rates, often by bundling paid family leave with other ancillary group benefits. Offering robust benefits packages that include dental, vision, accident insurance, group worksite benefits, long-term disability and group life / AD&D can help business owners recruit and retain top employees in a highly competitive environment.

Since business owners must begin collecting premiums for Colorado FAMLI by 2023, it’s important for brokers to start learning more about the Colorado business landscape and how they can help business owners implement this important program in the state.

You can rely on The DBL Center as your back-office staff to write private Colorado FAMLI benefits through our choice carriers.

[contact-form-7 id=”50050″ title=”Paid Family Leave Contact”] [/vc_column_text][/vc_column][/vc_row]